Has your business reached the point where you’re ready to hire more employees or expand into new customer markets? As your business becomes more complex, it may be time to revisit whether accrual accounting will be more effective for your financial and tax reporting.

In this post, we’ll go over what you need to know about the accrual method of accounting, including its benefits, how it compares to cash accounting, and if it’s right for your business.

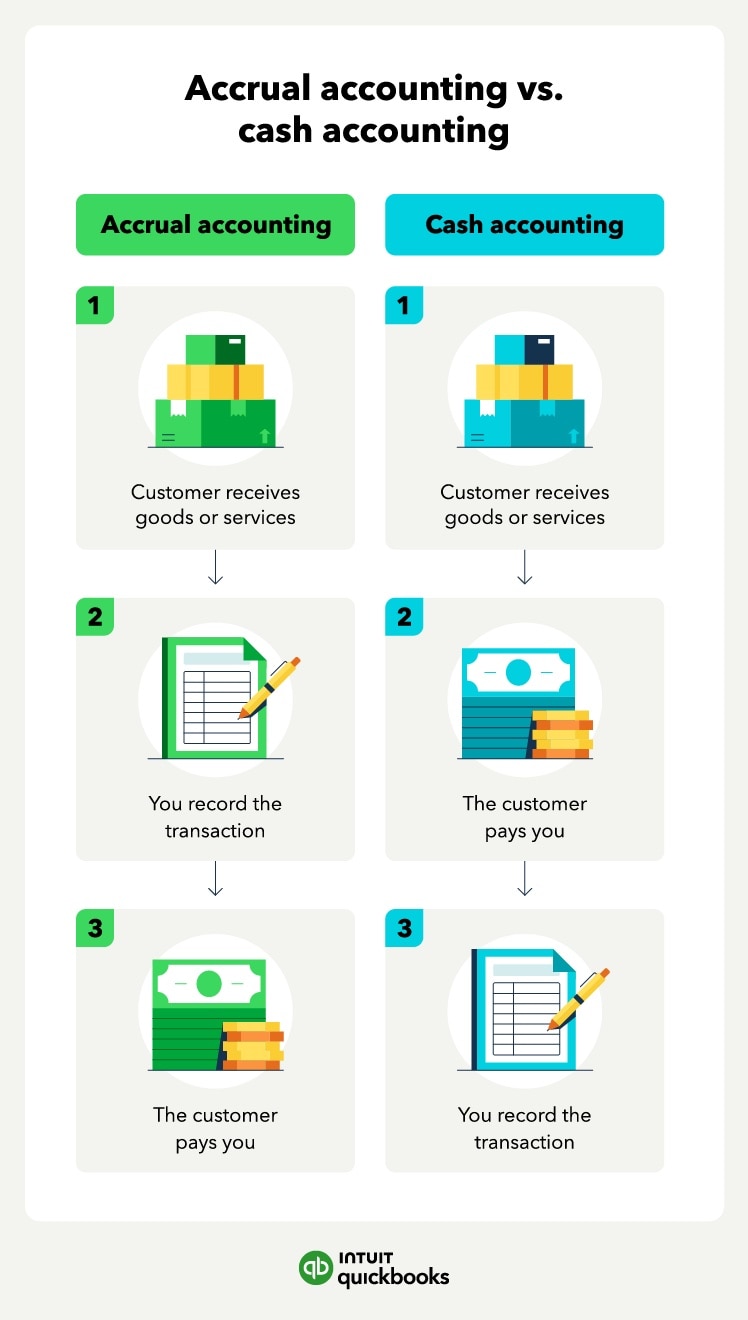

Though people commonly confuse accrual accounting with cash accounting, there are some stark differences to know before choosing which is right for your business.

Accrual-based accounting is a popular method for big companies, as it uses the double-entry accounting method, which is more accurate and conforms with the generally accepted accounting principles (GAAP).

In accrual accounting, you record income and expenses as you earn or incur them. This means you add income to your accounting journal when you complete a service or deliver goods and expenses when you receive an invoice for the goods and services.

Cash accounting, on the other hand, records income and expenses when you receive or deliver payment for goods and services. Most small businesses prefer the cash method because it’s simpler.

Here’s how they work: Let’s say your business provided a service to a customer in June, but they’ll only pay you in July. With accrual accounting, you’d record income for June, which is when you performed the service. But with cash accounting, you’d record income in July, when you received the payment.

Most businesses can choose between cash and accrual accounting methods. However, if an inventory is necessary to account for your income or your company’s income is over $25 million, the IRS will require you to use the accrual method.

When using accrual accounting, you’ll have different adjusting entries to add to the balance sheet and income statement .

These entries divide into two categories:

Let’s take a look at these types of adjusting entries and how you can use them in accrual accounting.

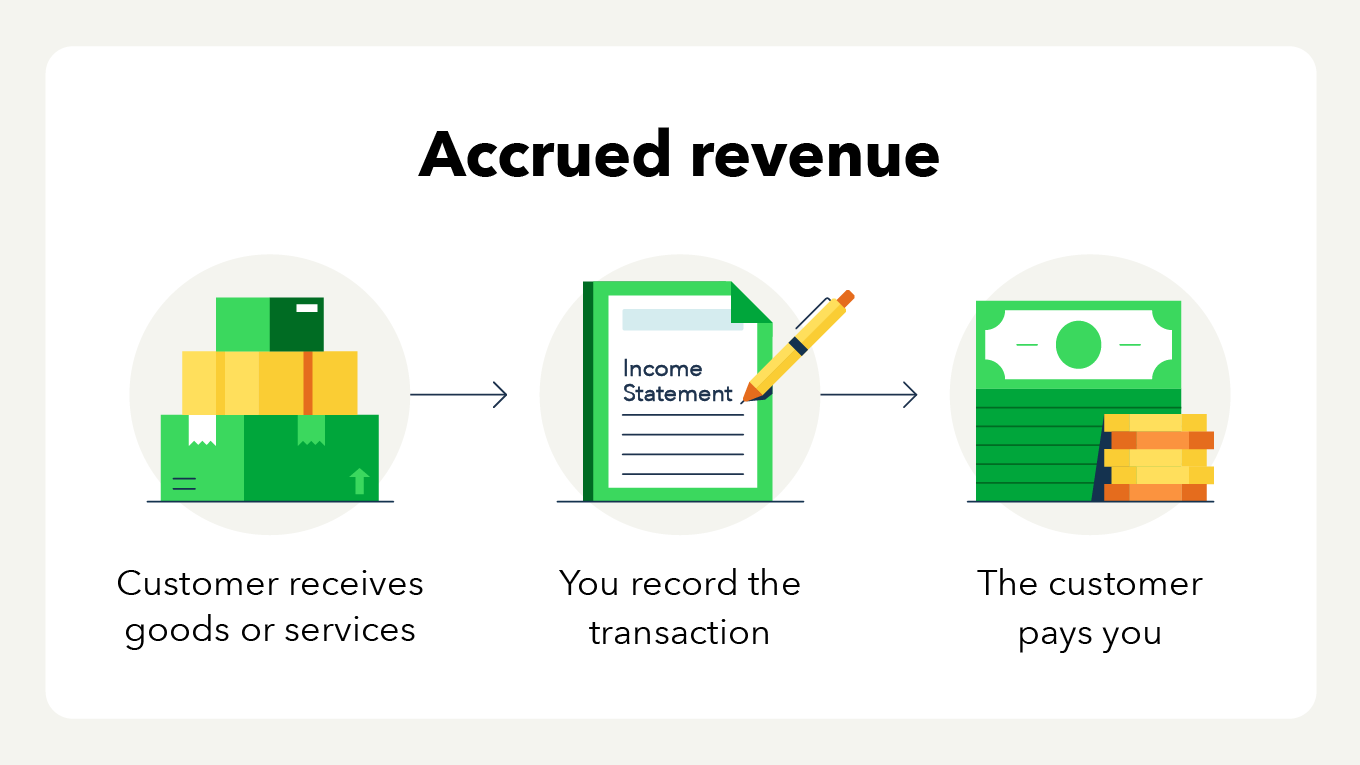

Accrued revenue is any income you expect to receive for any good or service you provided. It essentially means a customer owes you money for the transaction.

For example, if you provided a consulting service for $100 in January but you expect the customer to pay in February, you’ll have an accrued revenue of $100 in January.

In this case, you'd debit your accounts receivable and credit revenue . Here’s how you’d record this in January:

Then, in February, when you receive the payment, you’ll credit accounts receivable , which means receivables go down, and debits cash , which will go up.

Differently than accrued revenue, deferred revenues happen when a customer has paid for a good or service you haven’t yet provided. Meaning you owe the customer what they paid for.

This is common when customers pay for a subscription or have recurring payments , like a phone bill. For example, let’s say a customer paid $100 for your consulting services in January, but you’ll only be providing the service in February.

In this case, you would debit your cash account since it increased, and you'd credit your deferred revenue , which is a liability account. Here’s how you’d record this in January:

When you provide the consulting service in February, you’ll debit your deferred revenue , decreasing your liability. Then, you’ll credit revenue like so:

Accrued expenses are similar to accrued revenues in the sense that you were recording when the transaction happened, and not when there’s a payment. But in this case, your business is the one that has to pay.

This happens when you receive a good or service, but the provider expects you to pay at a later date. For example, let’s say you received merchandise for your business in March and received an invoice of $500 with payment due in April.

In accrual accounting, you’d record when you received the merchandise. In March, you’d debit $500 for expenses and credit accounts payable since you still have to pay for it. Here’s what it would look like:

Once you pay for the merchandise in April, you’ll debit accounts payable and credit cash :

Prepaid expenses are the opposite of accrued expenses. This means you already paid for the goods or services that you’re yet to receive. In this case, someone still owes you the goods and services you paid for.

For example, if you paid $500 for merchandise from your supplier in March, but they’ll only deliver them in April, you’ll have to debit the prepaid expense account and credit your cash account:

After you receive the merchandise in April, you’ll debit your expense account and credit prepaid expense :

Recording cash transactions based on when you complete services, deliver products, and incur expenses is also beneficial to your business.

Here are the main advantages typically associated with accrual accounting.

Still, it’s important to review the IRS guidelines on how to report an advance payment for services using the accrual accounting method.

Whereas accrual accounting’s strengths lie in accurately showing business profitability and representing long-term revenues and expenses, it has a few drawbacks as well.

Here are some pitfalls of accrual accounting:

Due to the added complexity and paperwork required under the accrual method of accounting, small business owners—particularly when starting a business —tend to view it as a less ideal option than the cash accounting method.

Accrual accounting provides a better picture of your overall financial position, and many companies consider it to be the standard and more accurate accounting method. But it can also be too complicated and expensive for small business owners.

One way to offset the people and time resources required under accrual accounting is to invest in accounting software that does the hard work for you.

Still have questions about accrual accounting? We’ve got the answers.

Accrual accounting is when you recognize a transaction in your journal entry when it happens instead of when you receive payment.

The basic rule of accrual accounting is to record transactions when they happen instead of when you receive or deliver payment.

The three accounting methods are cash basis accounting, accrual accounting and modified cash basis accounting, which combines cash and accrual accounting.

We provide third-party links as a convenience and for informational purposes only. Intuit does not endorse or approve these products and services, or the opinions of these corporations or organizations or individuals. Intuit accepts no responsibility for the accuracy, legality, or content on these sites.

**Product information

QuickBooks Live Assisted Bookkeeping: This is a monthly subscription service offering ongoing guidance on how to manage your books that you maintain full ownership and control. When you request a session with a Live Bookkeeper, they can provide guidance on topics including: bookkeeping automation, categorization, financial reports and dashboards, reconciliation, and workflow creation and management. They can also answer specific questions related to your books and your business. Some basic bookkeeping services may not be included and will be determined by your Live Bookkeeper. The Live Bookkeeper will provide help based on the information you provide.

QuickBooks Live Full-Service Bookkeeping: This is a combination service that includes QuickBooks Live Cleanup and QuickBooks Live Monthly Bookkeeping.

1. QuickBooks Online Advanced supports the upload of 1000 transaction lines for invoices at one time. 37% faster based off of internal tests comparing QuickBooks Online regular invoice workflow with QuickBooks Online Advanced multiple invoice workflow.

2. Access to Priority Circle and its benefits are available only to customers located in the 50 United States, including DC, who have an active, paid subscription to QuickBooks Desktop Enterprise or QuickBooks Online Advanced. Eligibility criteria may apply to certain products. When customers no longer have an active, paid subscription, they will not be eligible to receive benefits. Phone and messaging premium support is available 24/7. Support hours exclude occasional downtime due to system and server maintenance, company events, observed U.S. holidays and events beyond our control. Intuit reserves the right to change these hours without notice. Terms, conditions, pricing, service, support options, and support team members are subject to change without notice.

3. For hours of support and how to contact support, click here.

4. With our Tax Penalty Protection: If you receive a tax notice and send it to us within 15-days of the tax notice we will cover the payroll tax penalty, up to $25,000. Additional conditions and restrictions apply. See more information about the guarantee here: https://payroll.intuit.com/disclosure/.

Terms, conditions, pricing, special features, and service and support options subject to change without notice.

QuickBooks Payments: QuickBooks Payments account subject to eligibility criteria, credit, and application approval. Subscription to QuickBooks Online required. Money movement services are provided by Intuit Payments Inc., licensed as a Money Transmitter by the New York State Department of Financial Services. For more information about Intuit Payments' money transmission licenses, please visit https://www.intuit.com/legal/licenses/payment-licenses/.

QuickBooks Money: QuickBooks Money is a standalone Intuit offering that includes QuickBooks Payments and QuickBooks Checking. Intuit accounts are subject to eligibility criteria, credit, and application approval. Banking services provided by and the QuickBooks Visa® Debit Card is issued by Green Dot Bank, Member FDIC, pursuant to license from Visa U.S.A., Inc. Visa is a registered trademark of Visa International Service Association. QuickBooks Money Deposit Account Agreement applies. Banking services and debit card opening are subject to identity verification and approval by Green Dot Bank. Money movement services are provided by Intuit Payments Inc., licensed as a Money Transmitter by the New York State Department of Financial Services.

QuickBooks Commerce Integration: QuickBooks Online and QuickBooks Commerce sold separately. Integration available.

QuickBooks Live Bookkeeping Guided Setup: The QuickBooks Live Bookkeeping Guided Setup is a one-time virtual session with a QuickBooks expert. It’s available to new QuickBooks Online monthly subscribers who are within the first 30 days of their subscription. The QuickBooks Live Bookkeeping Guided Setup service includes: providing the customer with instructions on how to set up chart of accounts; customized invoices and setup reminders; connecting bank accounts and credit cards. The QuickBooks Live Bookkeeping Guided Setup is not available for QuickBooks trial and QuickBooks Self Employed offerings, and does not include desktop migration, Payroll setup or services. Your expert will only guide the process of setting up a QuickBooks Online account. Terms, conditions, pricing, special features, and service and support options subject to change without notice.